Are you juggling several loans and feeling overwhelmed by multiple monthly payments and high interest rates? You’re not alone.

Many people find themselves stuck in this cycle, wondering if there’s a smarter way to manage their debt. That’s where understanding multiple loan consolidation rates becomes a game-changer for your financial health. By consolidating your loans, you could simplify your payments and potentially lower your interest rates — freeing up cash and reducing stress.

Keep reading to discover how the right consolidation rate can help you take control of your debt and start saving money today.

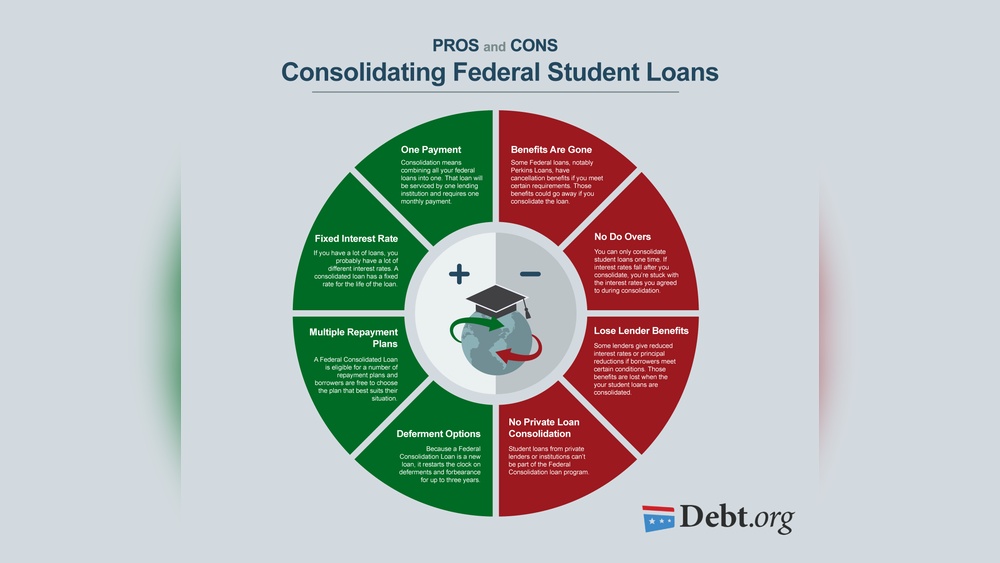

Benefits Of Loan Consolidation

Lower interest rates help save money on total payments. Consolidating loans usually means paying less interest than multiple separate loans.

Simplified payments mean you only pay once each month. This helps avoid missing due dates and reduces confusion.

Reduced financial stress comes from managing just one loan instead of many. It is easier to keep track of your debt and plan your budget.

How Loan Consolidation Rates Are Determined

Credit score plays a big role in setting loan consolidation rates. A higher score usually means a lower interest rate. Lenders see good credit as less risky.

Loan amount and term also affect the rate. Larger loans or longer terms might have higher rates. Shorter terms often get better rates but monthly payments can be higher.

Lenders have different rules and policies. Some offer fixed rates; others offer variable rates. Each lender’s terms can change the cost of consolidation.

| Factor | Effect on Rate |

|---|---|

| Credit Score | Higher score = lower rate |

| Loan Amount | Higher amount = possibly higher rate |

| Loan Term | Longer term = higher rate |

| Lender Policies | Varies by lender, fixed or variable rates |

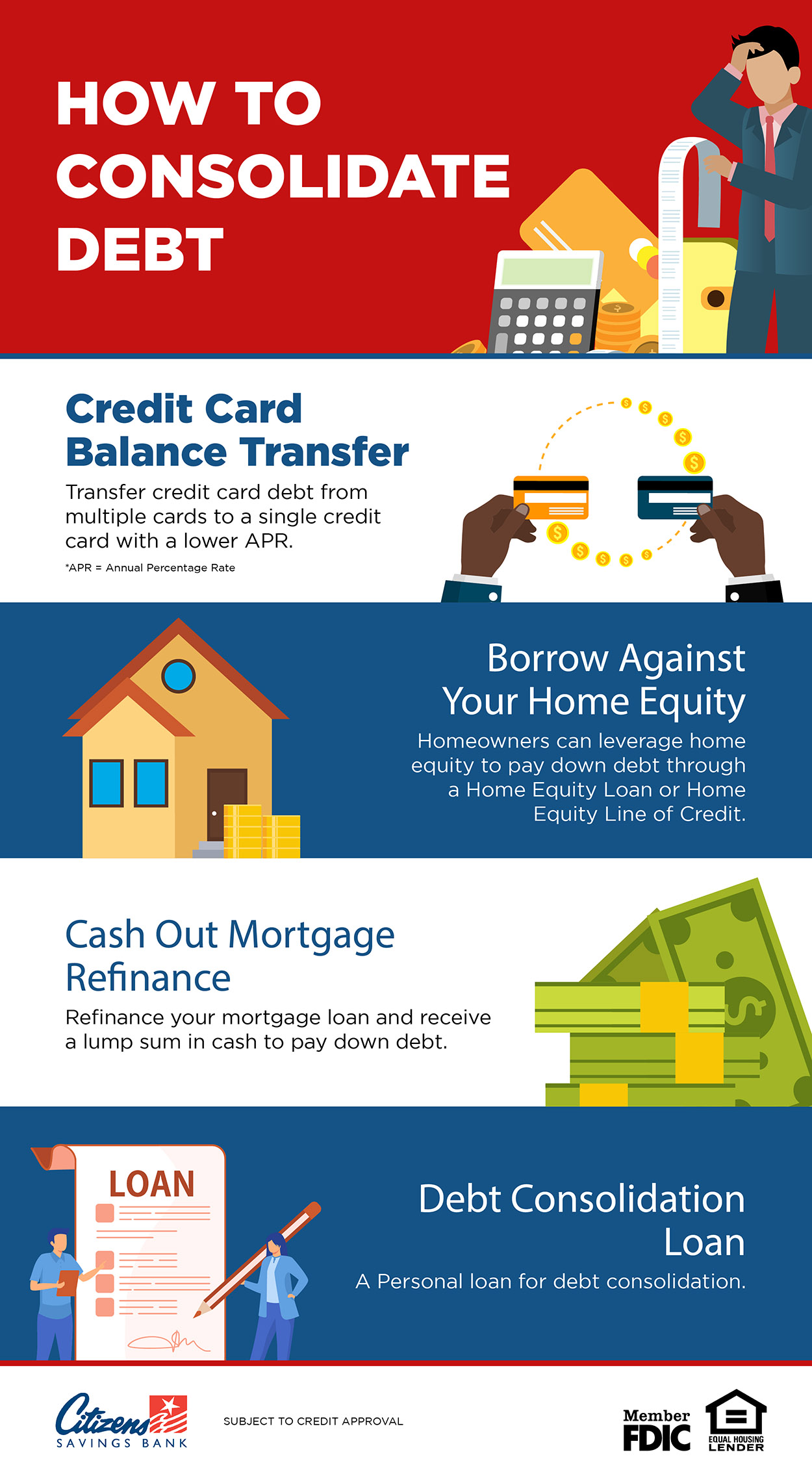

Types Of Consolidation Loans

Personal loans offer a simple way to combine debts. They usually have fixed rates and set terms. This helps with budgeting monthly payments. Interest rates can be lower than credit cards. But approval depends on your credit score.

Home equity loans use your house as collateral. They often have lower interest rates than personal loans. Payments can be spread over many years. However, failure to pay may risk your home.

Balance transfer credit cards let you move credit card debt to one card. Many offer a 0% introductory rate for a limited time. This can save on interest if paid off quickly. Watch out for transfer fees and higher rates later.

Comparing Multiple Loan Consolidation Rates

Fixed rates stay the same for the loan term. This means monthly payments never change. They give stability and make budgeting easier. Variable rates can go up or down based on market changes. They may start lower but can rise over time, causing payments to increase.

Many lenders offer promotional deals like lower rates for the first few months. These can save money early but watch for rate hikes later. Always read the fine print.

| Fee Type | Typical Cost | Details |

|---|---|---|

| Origination Fee | 1% to 5% | Charged when loan starts, reduces the loan amount |

| Prepayment Penalty | Varies | Fee for paying off loan early |

| Late Payment Fee | $25 to $40 | Charged if payment is late |

Compare these costs before choosing a loan. Even small fees affect total cost. Look at interest rates, fees, and terms to find the best deal.

Using Calculators To Estimate Savings

Debt consolidation calculators help you see potential savings. They work by asking for basic details about your loans. Common inputs include total loan amount, interest rates, and monthly payments. You might also enter the loan term or how long you want to pay it off.

After entering this information, the calculator shows your new monthly payment and total interest saved. It can compare your current loans to a single consolidated loan. This helps you understand if consolidation could lower your costs or simplify payments.

| Factor | Description |

|---|---|

| Total Loan Amount | The sum of all your current debts. |

| Interest Rate | The yearly cost of each loan expressed as a percentage. |

| Loan Term | How many months or years you plan to repay. |

| Monthly Payment | The amount you pay each month for your loans. |

Steps To Apply For A Consolidation Loan

Gather all financial documents such as pay stubs, bank statements, and loan details. These help prove your income and debts. Keep them organized for easy access.

Check your eligibility by reviewing credit score, income level, and debt amount. Different lenders have different rules. Knowing these saves time and effort.

Submit your application online or in person. Fill out forms carefully and attach required documents. Double-check for accuracy to avoid delays.

Common Pitfalls To Avoid

Ignoring loan terms can cause unexpected problems. Some loans have penalties for early payment. Others have variable interest rates that can rise later. Always read the fine print before signing. Know the exact monthly payment and total cost.

Overlooking fees is a common mistake. Many loans have hidden fees like origination charges or closing costs. These can increase your total debt. Ask the lender about all possible fees. Compare these fees with your current loans to see if consolidation saves money.

Extending loan terms excessively might lower monthly payments but can increase total interest. A longer loan means more interest paid over time. Choose a term that balances manageable payments with total cost. Avoid making your loan term too long just to lower monthly bills.

Tips To Maximize Savings

Improving your credit score can help you get lower consolidation rates. Paying bills on time and reducing debt balances boost your score. A higher score often means better loan offers. Keep credit usage low and avoid new debts before applying.

Choosing the right loan term is key. Shorter terms usually have lower interest rates but higher payments. Longer terms lower monthly payments but may cost more in interest. Pick a term that fits your budget and goals.

Negotiating better rates can save money. Compare offers from multiple lenders. Show your good credit and stable income. Ask for discounts or rate reductions. Small savings add up over time and lower your total loan cost.

Impact On Credit And Financial Future

Credit scores may rise or fall after loan consolidation. Paying off many loans with one payment can improve scores. But missing payments on a big loan hurts more. Keeping payments on time is key for good credit health.

Consolidation simplifies debt management. Instead of many bills, there is one monthly payment. This makes it easier to track and avoid missing deadlines. It may also lower the total interest paid over time, easing financial pressure.

Planning for the future becomes clearer with consolidation. Fixed payments help in budgeting monthly expenses. It can also free up money for savings or emergencies. This steady plan supports long-term financial stability and less stress.

Frequently Asked Questions

Is It Better To Consolidate Multiple Loans Into One?

Consolidating multiple loans into one can simplify payments and lower interest rates. It often reduces stress and saves money long-term.

What Is A Good Interest Rate For A Consolidation Loan?

A good interest rate for a consolidation loan typically ranges between 6% and 12%. Lower rates save money and reduce debt faster. Rates vary by credit score and lender. Always compare offers to find the best deal for your financial situation.

How To Pay Off $30,000 In Debt In 1 Year?

Create a strict budget, increase income, and cut expenses. Use debt consolidation loans for lower interest. Prioritize high-interest debts first. Make extra payments monthly to clear $30,000 within a year.

How Much Is The Payment On A $50,000 Consolidation Loan?

A $50,000 consolidation loan payment varies by interest rate and term. For example, at 8% over 5 years, monthly payments are about $1,013. Use a loan calculator for precise figures based on your rate and repayment period.

Conclusion

Choosing the right consolidation loan rate can ease your financial burden. Lower rates mean paying less interest over time. One simple monthly payment helps avoid missed due dates. Compare offers carefully to find the best fit for you. Keep track of terms and fees before deciding.

Consolidating loans can bring clarity and control to your finances. Think about your budget and long-term goals when selecting a loan. Taking action now can reduce stress and improve money management.