Are your monthly debt payments eating up too much of your paycheck? Imagine freeing up cash each month without changing your lifestyle or taking on new risks.

Lowering your monthly debt payments isn’t just a dream—it’s a smart move that can ease your financial stress and give you more control over your money. You’ll discover simple, effective ways to reduce what you owe every month. Ready to take the first step toward financial freedom?

Keep reading, because lowering your debt payments could be easier than you think.

Assess Your Current Debt

Start by listing all your debts. Include credit cards, loans, and other balances. Next, write down the interest rate for each debt. This helps to see which debts cost the most.

Calculate the total monthly payment by adding all minimum payments together. This gives a clear view of how much you pay each month.

Identify the debts with the highest interest rates. These are the ones that cost you the most money over time. Focus on paying these debts faster to save money.

Create A Realistic Budget

Start by tracking all income and expenses each month. Write down every dollar you earn and spend. This helps you see where money goes. Look for unnecessary expenses like eating out, subscriptions, or impulse buys. Cut these to free up cash.

Next, allocate money for debt payments before spending on wants. Prioritize debts with the highest interest rates. Pay at least the minimum on all debts to avoid fees. Extra payments reduce debt faster and lower total interest.

| Step | Action |

|---|---|

| Track Income | Record all sources of money each month |

| Track Expenses | List every spending item, including small purchases |

| Cut Spending | Remove non-essential expenses to save money |

| Allocate Funds | Set aside money for debt payments first |

Negotiate With Creditors

Request lower interest rates by calling your creditors. Explain your financial situation clearly and politely. Many creditors want to help and may offer reduced rates. This can lower your monthly payments significantly.

Ask for extended payment terms to spread out your debt over more months. This reduces each monthly payment amount, making it easier to manage. Be sure to confirm the new payment schedule in writing.

Explore hardship programs offered by creditors during tough times. These programs may pause payments, reduce interest, or lower monthly amounts temporarily. Check eligibility and apply directly through your creditor’s customer service.

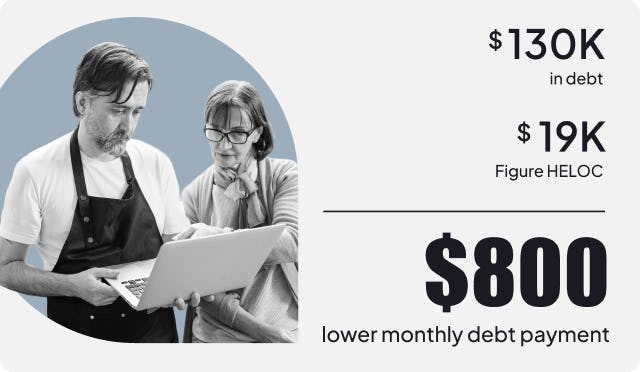

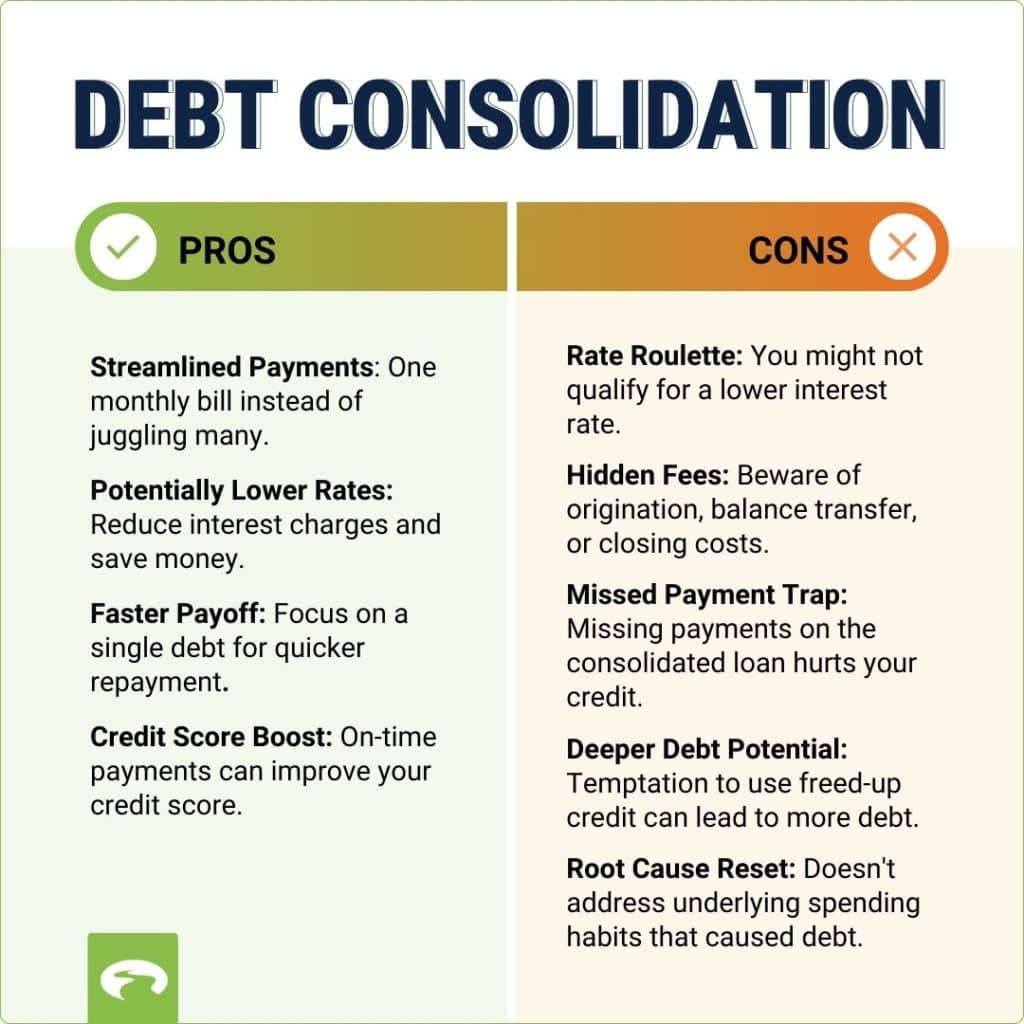

Use Debt Consolidation

Combining multiple debts into one loan can simplify payments. It helps to pay just one monthly bill instead of many. This approach often lowers the total monthly payment. Choosing a loan with a lower interest rate saves money over time. Comparing offers is key to find better rates.

Loan terms matter a lot. Look for longer repayment periods to reduce monthly costs. Check for any fees like origination or prepayment charges. Understanding these helps avoid surprises later. Always read the fine print before signing any loan agreement.

Try Debt Management Plans

Credit counseling services help create a debt management plan. They talk with your creditors to reduce interest rates and fees. You make one easy monthly payment to the agency. Then, the agency pays your creditors for you.

This plan simplifies payments and can lower your monthly bills. It may also protect you from late fees and collection calls. Be sure to ask about any fees for the service. Some plans take 3 to 5 years to complete.

| Benefits | Considerations |

|---|---|

| One monthly payment | May affect credit score |

| Lower interest rates | Requires discipline to pay monthly |

| Stops collection calls | Not all debts qualify |

| Works with your budget | Possible fees for service |

.png)

Apply Snowball And Avalanche Methods

The snowball method targets the smallest debts first. Paying off these quick wins builds confidence and momentum. It helps reduce the number of payments fast. This method is simple and motivating.

The avalanche method focuses on debts with the highest interest rates. Paying these first saves money on interest over time. It cuts debt faster but needs more discipline.

| Strategy | Focus | Benefit |

|---|---|---|

| Snowball | Smallest debts first | Quick wins and motivation |

| Avalanche | Highest interest debts | Save money on interest |

| Combined | Start small, then highest interest | Balance motivation and savings |

Combining both methods can be very effective. Start by clearing small debts to feel success. Then focus on high-interest debts to save money. This blend keeps you motivated and reduces total payments faster.

Explore Balance Transfer Options

0% APR credit cards can help reduce monthly debt payments by pausing interest charges for a set time. This means more of your payment goes toward the principal balance, lowering the total owed faster.

Watch out for transfer fees. Most cards charge a fee, usually 3% to 5% of the amount moved. Compare these fees to potential interest savings to see if the transfer is worth it.

Plan your payments carefully before the 0% APR period ends. Interest rates will rise, increasing monthly costs. Aim to pay off as much debt as possible during the no-interest time to avoid extra charges.

Automate And Prioritize Payments

Setting up automatic transfers helps pay bills on time every month. This avoids late fees that add extra costs. Your bank can send money to your creditors automatically. This keeps your credit score healthy.

Try to increase payments whenever you can. Even small extra amounts reduce debt faster. Prioritize paying off debts with the highest interest first. This saves money over time.

Organize your payments by importance. Pay essential bills first, like rent and utilities. Then, focus on debts that charge late fees. Automating payments reduces stress and keeps you on track.

Seek Professional Advice

Financial advisors can help create a plan to lower monthly debt payments. They review income, expenses, and debts to find the best options. Debt settlement may lower what you owe, but it can hurt your credit score. Think about all risks before agreeing to settle.

Legal help is useful if debt collectors act unfairly or if bankruptcy seems necessary. Lawyers explain rights and guide through complex processes. Getting advice early can prevent bigger problems later. Professional help makes managing debt less stressful and more effective.

Frequently Asked Questions

What Is The 7 7 7 Rule For Debt Collection?

The 7 7 7 rule for debt collection means contacting debtors every 7 days, for 7 weeks, using 7 different communication methods. This strategy increases chances of successful debt recovery.

How To Get Rid Of $30,000 In Debt Fast?

Create a budget, prioritize high-interest debts, and pay extra monthly. Use debt snowball or avalanche methods. Consider debt consolidation or credit counseling to lower payments and speed up repayment.

What Is The 15 3 Payment Trick?

The 15 3 payment trick involves paying $15 every 3 days to reduce debt faster. This method lowers interest and speeds up repayment.

What Is The 50 30 20 Rule For Debt?

The 50 30 20 rule for debt allocates 50% of income to needs, 30% to wants, and 20% to debt repayment or savings.

Conclusion

Lowering your monthly debt payments can ease financial stress. Start by reviewing all your debts carefully. Consider options like debt consolidation or negotiating with lenders. Small changes in spending habits also help. Stay consistent and track your progress each month.

Reducing payments frees money for savings or emergencies. Keep focused on your goal and take action today. You deserve a lighter financial load and peace of mind.