Thinking about applying for a loan but worried about how it might affect your credit score? You’re not alone.

Many people hesitate to check their loan options because a hard credit pull can lower their score. That’s where a Soft Pull Loan Precheck comes in—a simple way to see your potential loan offers without any risk to your credit.

Imagine knowing your chances before you commit, giving you the power to make smarter financial decisions. Keep reading to discover how a soft pull works, why it matters to you, and how it can make your loan search easier and less stressful. Your path to a better loan starts here.

Soft Pull Loans Basics

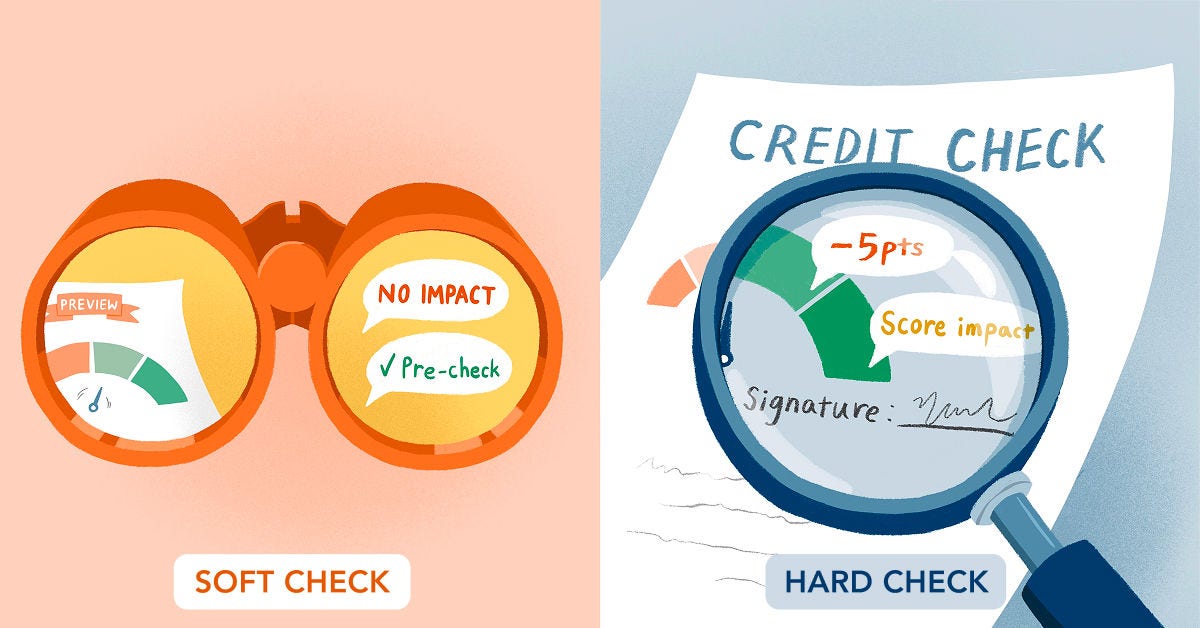

A soft pull is a type of credit check that does not affect your credit score. It allows lenders to see some of your credit information without a full review. This is useful for prequalifying loans or credit cards.

A hard pull happens when a lender fully checks your credit to make a final decision. Hard pulls can lower your credit score slightly and stay on your report for two years.

| Soft Pull | Hard Pull |

|---|---|

| Does not affect credit score | Can lower credit score |

| Used for prequalification | Used for final approval |

| Visible only to you on credit report | Visible to all lenders on credit report |

Benefits of soft pull loans include no impact on your credit score and easy prequalification. They help you compare offers without risk. This saves time and stress in the loan process.

How Soft Pull Prechecks Work

Credit Report Access through a soft pull lets lenders view your credit without full permission. This type of pull only shows limited details. It helps lenders decide if you might qualify for a loan.

The Prequalification Process uses soft pulls to quickly check if you meet loan criteria. It saves time and avoids hard inquiries that can hurt your credit score. Many lenders offer prequalification online with soft pulls.

| Impact on Credit Score | Soft Pull | Hard Pull |

|---|---|---|

| Effect on Score | No effect | May lower score by a few points |

| Visibility | Visible only to you and lenders for prequalification | Visible to all lenders checking your credit |

| Usage | Used for prechecks and background checks | Used when applying for loans or credit cards |

Finding Soft Pull Loan Options

Soft pull loans let you check loan options without hurting your credit score. Lenders use a soft credit check to see if you qualify. This helps you compare offers easily.

Online lenders often provide quick soft pull prechecks. They use automated systems and give instant results. Traditional lenders, like banks or credit unions, may also offer soft pull loans but usually take longer to respond.

| Type of Lender | Soft Pull Offer | Response Time | Regional Availability |

|---|---|---|---|

| Online Lenders | Common | Fast (minutes) | Nationwide |

| Traditional Banks | Less common | Slower (days) | Regional/Local |

| Credit Unions | Sometimes | Moderate | Regional |

Some lenders serve specific regions. Check lender availability in your area to save time. Soft pull loan options vary by location and lender type.

Preparing For A Soft Pull Loan

Checking your credit health helps you understand your loan chances. Review your credit report for errors or negative marks. Fix any mistakes to improve your score. Knowing your credit score range sets realistic expectations.

Gather necessary documents before applying. These include pay stubs, tax returns, ID, and bank statements. Having these ready speeds up the loan process. Lenders need them to verify your income and identity.

Improving eligibility can boost loan approval odds. Pay down debts and keep credit card balances low. Avoid opening new credit accounts just before applying. Consistent income and stable job history also help your case.

Tips For Quick Approval

Choosing the right lender helps speed up your loan approval. Pick lenders who offer soft pull loan prechecks. This means they check your credit without lowering your score. Avoid lenders that only use hard credit pulls early on.

Submitting accurate information is key. Double-check all personal details before sending. Mistakes slow down the process and cause delays. Provide clear and complete documents to help lenders verify quickly.

Responding to requests promptly shows you are serious. Answer emails and calls fast. Missing deadlines or ignoring messages can hold back your approval. Keep your phone handy and check your email often.

Avoiding Risks With Soft Pull Loans

Recognizing scams is very important when dealing with loans. Always check if the lender is licensed and has good reviews. Beware of offers that seem too good to be true. Never share sensitive information like your Social Security number without verifying the lender’s identity. Scammers often ask for upfront fees or pressure you to act fast.

Understanding loan terms helps avoid confusion. Look closely at the interest rate, monthly payments, and loan length. Ask questions about any fees or penalties. A soft pull loan lets you see your rate without hurting your credit score.

Monitoring your credit regularly is smart. Check your credit report for errors or unfamiliar accounts. Soft pulls do not affect your credit score, so you can check offers safely. Keep track of your credit to catch problems early.

Using Soft Pull Loans Wisely

Soft pull prechecks help you see loan options without hurting your credit score. They let you compare multiple offers easily. Use soft pulls before applying to avoid hard inquiries that can lower your score.

These checks are perfect for comparing loan offers. You can see interest rates, fees, and terms from different lenders. This helps you pick the best deal without risk.

Planning repayment is easier with soft pulls. You know your likely loan terms in advance. This helps you budget and avoid surprises later. Keep track of loan details to stay on top of payments.

Frequently Asked Questions

What Is A Soft Pull Loan Precheck?

A soft pull loan precheck is a credit check that doesn’t affect your credit score. It helps lenders prequalify you for a loan by reviewing your credit report softly. This process gives you an idea of loan options without a hard credit inquiry.

How Does A Soft Pull Differ From A Hard Pull?

A soft pull does not impact your credit score, while a hard pull can lower it. Soft pulls are used for prequalification and informational purposes. Hard pulls occur when you apply for credit and can affect your credit rating.

Can A Soft Pull Precheck Approve My Loan?

No, a soft pull precheck only prequalifies you. It gives an estimate of loan eligibility and rates. Final approval usually requires a hard credit pull and additional verification by the lender.

Will A Soft Pull Affect My Credit Score?

No, soft pulls do not affect your credit score. They are visible only to you and the lender performing the precheck. This makes soft pulls safe for checking loan options without damaging your credit.

Conclusion

Soft pull loan prechecks help you explore loan options without hurting your credit. They show potential rates and eligibility quickly and simply. Using a soft pull keeps your credit score safe during your search. This makes comparing loans easier and less stressful.

Keep soft pulls in mind when planning your next loan. They offer a smart way to learn before you commit.